Borrowers Section 184 Loan Resources

Are You Ready for Homeownership?

Purchasing a home is one of the biggest financial decisions you will make in your lifetime, so it’s critical to prepare yourself in advance. The following steps are intended to help you get started. Download "Are You Ready for Homeownership?" flyer.

Educate yourself on the homebuying process or take a free homebuyer education class. Check with your tribe to see if they provide classes and/or check with a HUD-approved Counseling Agency at: www.hud.gov/counseling

Do a self-assessment.

Income—do you have adequate and stable income? Do you have a two year employment history?

Credit—Have you reviewed your credit report recently? Is it accurate? You can order a free copy at: www.annualcreditreport.com

Debt—Student loans, car loans, credit cards, personal loans all are included in your monthly debt ratio. If needed work to pay off debts.

Down payment—You’ll need 2.25% to cover the cost of your down payment. Check with your tribe or the state Housing Finance Agency to see what they provide. Ensure you have additional funds to cover closing costs.

Tribal Trust or Allotted Lands—Do you own your own land? Are you the only owners of record? Does the property have infrastructure? Allotted: Order a title status report to see owners listed; Trust: Check with your tribe about getting a lease.

If you’ve covered all of the above check-in with a Section 184 approved lender. You can find a list of approved lenders here. The lender will explain the loan approval process to you and request numerous documents that are needed to complete your loan file. Follow up quickly to ensure the loan process is not delayed.

TIPS:

Develop a budget that includes your anticipated loan payment, utility costs, and other monthly payments. Will you still have funds left over for savings and a maintenance fund?

Do not take on any new debt if you are planning to purchase a home. It will add to your debt to income ratio and lower the amount of home loan you might qualify for.

Review Training on Section 184 Basics: Qualifying for a Section 184 Indian Home Loan

"We are in a home that we built from the ground up. It's hard to describe the experience of building a home... It's a difficult process, but in the end, it's one of the most amazing accomplishments you'll ever achieve."Gena, Makah Tribe |

What is the Section 184 Loan Guarantee Program?

The Section 184 Loan Program was designed to provide access to mortgage financing to Native American and Alaskan Native tribal members. Section 184 home loans are guaranteed 100% by the Office of Loan Guarantee within HUD's Office of Native American Programs.

This guarantee encourages national and local banks to provide mortgage loans to Native Americans. The Office of Loan Guarantee works with a national network of lenders to increase Native access to home financing and to improve the value of Native investments.

Why Should I Use the Section 184 Loan?

There are many advantages to using a Section 184:

Low Down Payment: 2.25% on loans over $50,000 and only 1.25% on loans under $50,000

Low Interest Rates: based on market rates, not on applicant’s Credit Scores

Manual Underwriting: The Program utilizes a hands-on approach to underwriting and approval opposed to automated decision-making tools.

Growing National Network of Approved Lenders: Our network of approved lenders includes national companies and local banks to suit your needs. Our Lenders have also been trained on the unique circumstances of Native homeownership.

Section 184 Upfront Loan Guarantee Fee: A one-time 1% up front guarantee fee is paid at closing and can be financed into the loan. For loans closed on or after July 1, 2023, there is no Annual Loan Guarantee Fee.

Protection from predatory lending: Our Program monitors the fees our approved lenders can charge Native borrowers. Section 184 loans cannot be used for Adjustable Rate Mortgages (ARMs).

Knowledgeable Staff: Our staff understands the unique circumstances associated with lending on Native Lands and we work with borrowers to achieve home ownership and to avoid default and foreclosure.

What Can I use the Section 184 Loan for?

You can use the Section 184 Loan to:

Purchase an Existing Home

Construct a New Home (Site-Built or Manufactured Homes on permanent foundations)

Rehabilitate a Home, including weatherization

Purchase and Rehabilitate a Home

Refinance a Home (Rate and Term, Streamline, Cash Out)

Section 184 loans can only be used for single family homes (1-4 units) and for a primary residence. Since 184 strives to increase homeownership to all Native Communities, the guarantee funds are reserved for primary residences rather than second or investment properties.

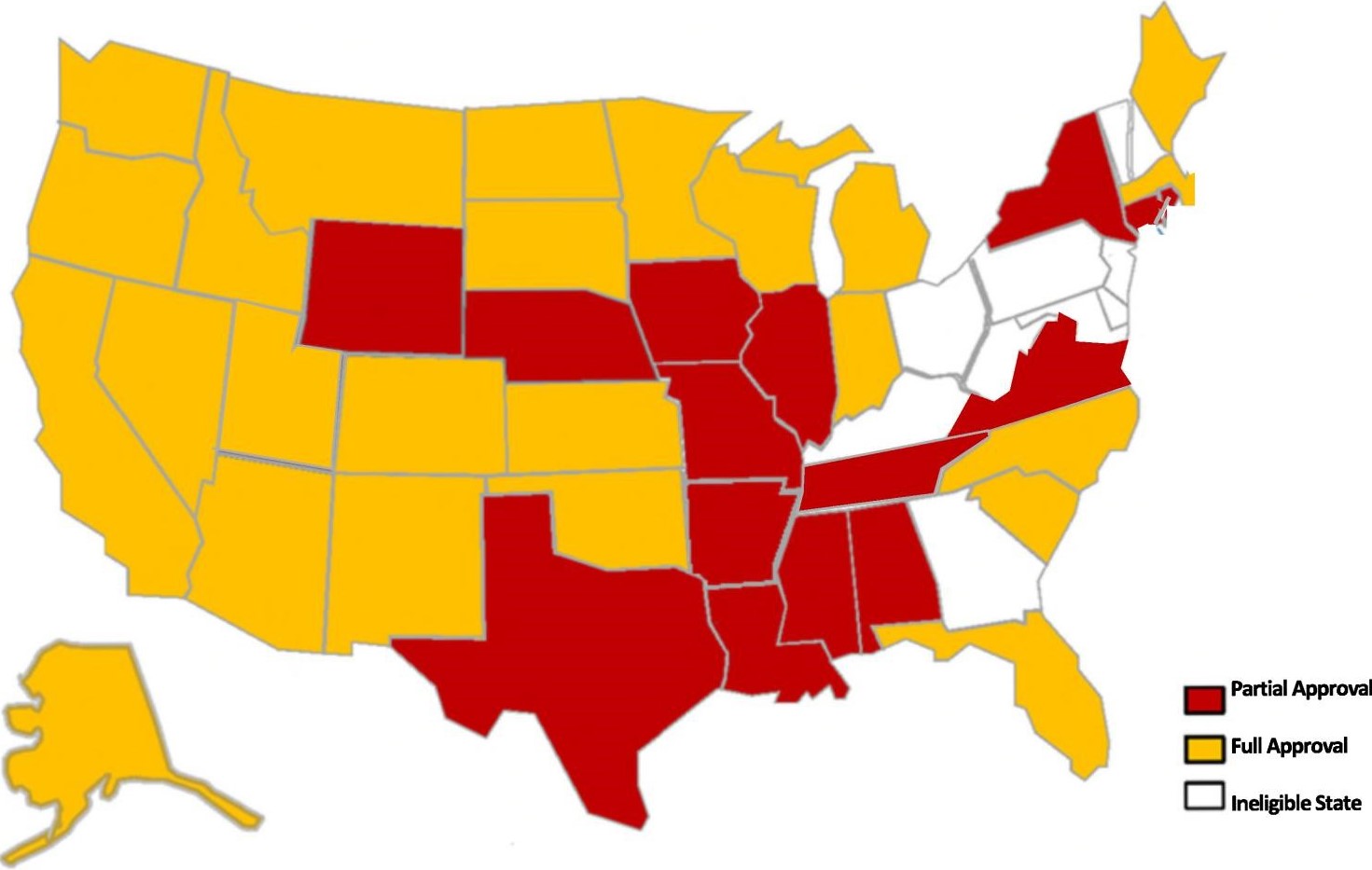

Where can I use the Section 184 Loan?

Participating Tribes determine the areas where the Section 184 loan can be used. Loans must be made in an eligible area. The program has grown to include eligible areas beyond tribal trust land. Click on the links below to determined participating States and counties across the country.

Tribal Enrollment

To use the Section 184 Loan, you must be a currently enrolled member of a Federally Recognized Tribe.

Verification of enrollment will be required when applying for a Section 184 loan. Neither Section 184 nor our approved lenders can assist in this enrollment process. Contact your tribe for their enrollment requirements.

Homebuyer Education

Before meeting with a lender, it is recommended that you prepare for the home buying process by attending a homebuyer class or counseling session. Understanding what it takes to qualify for a loan can help you prepare for meeting with a lender.

Although these classes are not mandatory, they are greatly beneficial to you. Some lenders or Tribes will even offer financial assistance to borrowers who attend these classes.

Find an Approved Section 184 Lender

Once you are ready to apply for a Section 184 loan, contact one of our approved lenders. All of our approved lenders have undergone training on the unique circumstances of Native Homeownership.

Other Resources

Are you a Lender or CDFI? View Lender Resources.

Are you a Tribe or TDHE? View Tribal Resources.